Is a Reverse Mortgage a Tool or a Trap?

The truth? It depends on what you know before you decide.

This guide offers a clear, unbiased breakdown of how reverse mortgages work, when to use them, and when to avoid them.

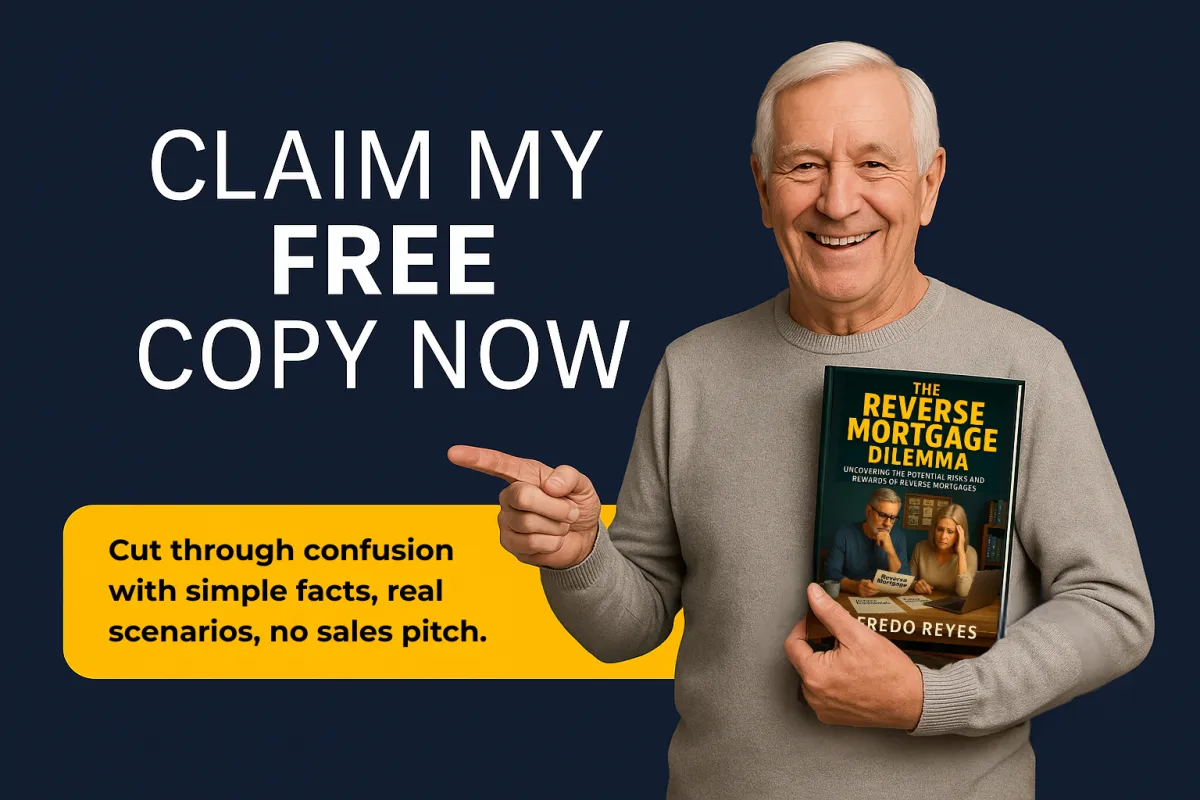

👉 Download The Reverse Mortgage Dilemma. Free to the first 250 this month.

Use Our Free Proprietary Reverse Mortgage Calculators

We're Not Selling You a Loan.

We're Handing You the Whole Playbook.

If you're 55 or older, a reverse mortgage might be a powerful retirement tool or a costly misstep.

Our guide, paired with our proprietary Reverse Mortgage Calculators, helps you see the real numbers behind the decision with real retiree experiences, independent research, and a clear explanation of how reverse mortgages actually work.

Sources You Can Trust

What’s Inside The Reverse Mortgage Dilemma

✅ A breakdown of how reverse mortgages actually work (without the sales pitch)

✅ Common traps lenders don’t explain — and how to avoid them

✅ Real-life retiree case studies (good and bad)

✅ Clear decision checklists for you and your family

Trusted by professionals in finance, planning, real estate, and senior care.

Clarity over confusion.

What it Is and Isn’t

Understand exactly how a reverse mortgage works, without sales pressure or scare tactics.

The Real Risks

Learn what can go wrong, what protections exist, and how to spot red flags before it’s too late.

When It Helps

See examples of how some homeowners have used it to improve their financial situation.

When to Avoid It

Learn the clear situations where a reverse mortgage may do more harm than good.

Straight from the Source

Every claim is backed by research from HUD, CFPB, AARP, and independent studies so you can trust what you’re reading.

Read Before You Decide

This book doesn’t sell or persuade. It gives you the facts so you can choose with confidence.

Testimonials

“I always thought reverse mortgages were a scam. This book didn’t sell me. It just gave me the facts. I finally feel like I understand what’s really at stake.” — Eleanor M., 72

“Clear, calm, and exactly what I needed. I’ve seen so many scary headlines, but this book helped me think through it logically, not emotionally.” — Janet L., 75

“After reading this, I didn’t jump into a loan. I had a real conversation with my kids and my advisor. I feel way more confident about my options now.” — Ron S., 68

“My lender gave me the rosy version. This book filled in the blanks and showed me what to watch out for. Very helpful.” — George K., 70

A Look Inside Reverse Mortgage Dilemma

Real Concerns. Real Scenarios. Zero Sales Pitch.

Separating Fact from Fear

If you’re feeling overwhelmed by negative headlines or warnings from friends, this chapter explores how to separate inherited fears from actual risks.

Chapter 1

Navigating the Information Maze

When online research only leads to more confusion, this chapter offers a simple framework for making sense of the noise.

Chapter 2

When the Experts Change Their Minds

Some advisors oppose reverse mortgages. Others have changed their views. This chapter looks at why professional opinions have shifted and what it means for you.

Chapter 3

Social Security Bridge Strategy

If you’re thinking about delaying Social Security but need income now, this chapter explores different ways people fill that gap.

Chapter 4

Eliminating Payment Anxiety

When mortgage payments are causing monthly stress, this chapter shows what options homeowners have explored to find relief.

Chapter 5

Aging in Place with Confidence

For those who want to stay in their homes but need funds for safety upgrades or in-home care, this chapter explores possible paths forward.

Chapter 6

Relocating in Retirement

If moving closer to family or downsizing feels out of reach financially, this chapter walks through creative ways others have tackled that challenge.

Chapter 7

Understanding Your Responsibilities

Many borrowers worry about what they might be missing. This chapter breaks down what it really takes to stay in good standing with a reverse mortgage.

Chapter 8

Protecting Your Family’s Inheritance

If family reactions or legacy concerns are weighing on you, this chapter explores how others have balanced emotional and financial priorities.

Chapter 9

Avoiding Predators and Scams

With so many bad actors in the space, this chapter gives you tools to recognize who’s credible and who isn’t.

Chapter 10

The Counseling Experience

This chapter explains what to expect from the required reverse mortgage counseling, helping reduce nerves and uncertainty.

Chapter 11

Your Complete Action Plan

A reflection tool to help you organize your thoughts, whether you're just getting started or ready to explore your options in depth.

Chapter 12

Frequently Asked Questions

What exactly is a reverse mortgage?

A reverse mortgage is a loan available to homeowners (typically age 55 or older) that lets them tap into the equity in their home without making monthly mortgage payments. The loan balance is repaid when the homeowner moves out, sells the home, or passes away.

Is a reverse mortgage a scam?

No — it’s a legitimate financial product. But like any loan, there are pros, cons, and risks. Many lenders don’t fully explain cost traps, fees, or what happens to inheritance. Our book aims to show the full picture so you can make an informed decision without being misled.

Who is a reverse mortgage good for — and when should I avoid it?

-When it might help: If you’re older, own your home (or have high equity), and need income or funds for health, aging-in-place modifications, or delayed Social Security strategies.

-When it may be risky: If you plan to move soon, want to leave the house as inheritance, or if costs/fees outweigh benefits in your situation. Also risky if you’re not clear on your obligations (taxes, insurance, upkeep).

What are the hidden risks or traps lenders sometimes gloss over?

Common issues include high fees, interest compounding over time, lender misrepresentation, loss of home if property obligations (taxes, insurance, maintenance) aren’t met, or unexpected costs when you or your heirs sell. Our book walks through real case studies to expose what often isn’t said.

How does this book help me decide whether a reverse mortgage is right for me?

-A clear explanation of how reverse mortgages work, without pressure or sales pitches.

-Real-life case studies, both positive and negative, so you can see how outcomes vary.

-Decision checklists to walk through your priorities and risks.

-Tools to understand what obligations come with having a reverse mortgage.

Do I need professional advice or counseling?

Yes. In many cases, reverse mortgages require HUD-approved counseling. It helps you understand the legal, financial, and family implications, and evaluate whether it’s the best fit. Our book explains what to expect from this process.

Will taking out a reverse mortgage affect inheritance or what I leave behind?

It can. Because the loan balance grows over time (from interest and fees), there may be less equity left in the home at the end. Our book includes a section on protecting your family’s inheritance and how to align the loan with your legacy goals.

How do I spot scams or unscrupulous lenders?

Look for transparency: Are all fees disclosed clearly? Are they rushing or pressuring you? Are they explaining counseling and legal disclosures? Do the numbers add up? Our book includes tools and red-flag checklists to help you evaluate lenders with confidence.

Disclaimer: For Educational Purposes Only

The information, tools, and calculators provided on Reverse Mortgage Dilemma are intended solely for educational and informational purposes. They are designed to help you better understand how a reverse mortgage might align with your retirement goals. This content is not intended to serve as financial, legal, or tax advice.

All materials are developed and reviewed by Reverse Mortgage Experts with decades of combined experience in mortgage lending, underwriting, and real estate. However, every financial situation is unique. We strongly recommend consulting with a qualified financial advisor, tax professional, attorney, Reverse Mortgage Advisor or a HUD-approved housing counselor before deciding related to reverse mortgages.

To ensure accuracy and reliability, our educational content references well-established, nationally recognized sources, including HUD, CFPB, AARP, and other authoritative organizations in retirement and housing.

Our mission is to provide unbiased, clear, and helpful information so that you can make confident and informed decisions about your financial future.

Email: [email protected]